When was the last time you heard a product was in demand? What did it mean? It could have been a novel product or an existing one with fantastic pricing or simply well-marketed. Or it could be all three and more.

As demand for a product increases, so should the supply. Not doing so results in lost revenues. Conversely, if it drops or ceases to exist, supply must match up. Else, the supply chain will clog up with excess unsold inventory. Simple? Not quite.

All of this give and take happens in a marketplace – where supply meets demand. Here several variables come into play like price, competition, seasonality, macroeconomic conditions, and willingness of a consumer to pay. They influence both demand and supply of a product.

Let’s simplify this further.

Table of Contents

How do you define Supply and Demand?

- Supply is the quantity of a product that a business – manufacturer or service provider – makes available for its customers at a specific price

- Demand is the quantity of a product that customers are willing to purchase at a specified price

What are the fundamental differences between Supply and Demand?

For starters, supply is a seller-side function. The ideal supply quantity matches the demand. However, it depends on several factors; the predominant one is cost. It takes money to make a product and also to market and distribute it.

If you are a small company and have just launched a stellar product, taking it to a larger market will involve higher expenses. You will have to market, transport, and distribute in the new locations. If the demand increases, you will have to invest in expanding your production capacities. You may also have to hire more people to meet the new requirement.

Thanks to the hard determinants, you can calculate the investment required to produce x quantity. However, deciding on the x quantity isn’t as easy because demand depends on softer aspects and has an element of unpredictability attached to it.

Demand planning takes time, effort, and analysis of data. Moreover, the data needs to be analyzed considering external variables that impacted sales in previous years.

For example, consumer spending patterns for office wear would have drastically changed in the pandemic years. Understandably, working from home, most people wouldn’t have felt the need for it. Similarly, the demand for expensive watches and jewelry must have also taken a hit. In the post-pandemic year, therefore, demand forecasting must account for changing consumer behavior.

Relationship of Demand and Supply with pricing – Demand curve and Supply Curve

Pricing is intricately related to demand and supply – it influences and impacts demand and supply. Here we discuss how.

A product is unlikely to experience significant demand if it is priced much higher than

- Competition

- Perceived value

- Affordability of its target consumer segment

At a higher price, the quantity of demand will always be less. A price drop propels demand. The following demand curve depicts the relationship between price and quantity.

On the other hand, at lower quantities, the cost of production is also less. The supply curve below shows the relationship between cost and quantity.

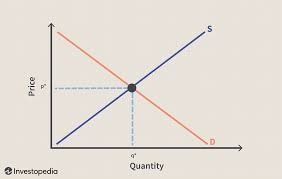

So, demand and supply, although dynamic, operate within a set of laws.

Laws of Supply and Demand

- Increased supply at constant demand results in a lower price and higher quantity.

- Decreased supply at a given level of demand leads to a higher price and lower quantity

- Increased demand at constant supply results in a higher price and higher quantity

- Decreased demand at a given supply level leads to a lower price and lower quantity

Digging a little deeper – exploring Supply-side and Demand-side economics

From an economic perspective, there exist different schools of thought on whether supply or demand drives growth.

The proponents of classical economics believe that increasing the supply of goods leads to economic growth. Reduction of taxes, lowering borrowing rates, and deregulation of industries are some measures towards boosting supply. It’s commonly referred to as supply-side economics. Demand-side economics, on the other hand, is a Keynesian economics belief. It advocates demand for goods and services drives economic growth. In essence, these two theories try to explain the economic impact of demand and supply.

The problem occurs when there’s too much of either Supply or Demand

When demand for a product outstrips its supply and has consumers willing to pay a premium, it will command a higher price in the market. Whereas, if supply is far greater than demand, the prices go down. It could be in the form of temporary discounts or a long-term price correction.

A competitive market provides multiple options to the consumer. As the options increase, the aggregate supply of a product increases. When the supply of similar products from different brands exceeds the aggregate demand for the product, the prices must reduce. Further, as price becomes the primary factor influencing the purchase decision, the brands are forced to undercut the competition to clear surplus stocks.

While offering a product at a high price has its downsides, extremely low pricing also is a problem. It creates an unanticipated surge in demand. As the businesses produce more of a good, the production and supply chain costs shoot up. A low-priced product may not be able to cover all of it.

Achieving equilibrium is the key to success

To avoid being stuck with unsold inventory or getting caught up in the downward pricing spiral, a business must invest in efficient demand forecasting and supply planning. The objective of this exercise must be to achieve a demand-supply equilibrium. It entails offering a product at a price that matches the consumer’s budget. At the same time, it shouldn’t sacrifice profitability. However, it’s easier said than done.

Final Thoughts

Given the number of variables, amount of data, and the complexity of the planning process, businesses rely on software applications. From predictive analytics tools to artificial intelligence, several solutions exist in the market. The choice of the software depends on the size of the business, geographical footprint, number of SKUs, among other factors.

Looking for a pro-tip? When picking a software solution, look at the cost savings of efficient forecasting and inventory planning rather than the cost of the standalone solution. Check out the leading inventory management software solutions available in the market today.